“Busy But Not Profitable? You’re Stuck in the Wrong Part of the Value Triangle”

Listen to the Audio version of this blog here.

Watch a brief summary video of this blog.

1. Introduction – The Lie Most Buyers Believe

I hear it all the time.

“We need it done quickly… done properly… and at the best possible price.”

On the surface, that sounds reasonable. In fact, it sounds like good business. Who wouldn’t want speed, quality, and low cost all at the same time? But here’s the reality I’ve learned after years of working with business owners, contractors, and service providers:

That expectation is a lie.

Not because people are being unreasonable but because they’re asking for something that simply doesn’t exist.

Where This Shows Up in the Real World.

Let me give you a few examples you’ll recognise straight away.

Example 1: The Cheapest Quote Wins

A business puts a job out to tender. Three quotes come back:

- £120,000

- £105,000

- £78,000

They choose £78,000.

On paper, it looks like a win. Same job, lower price.

But what they don’t see (yet) is:

- Missing scope

- Vague allowances

- Corners that will have to be cut

Six months later, the job is over budget, behind schedule, and full of friction. They didn’t get cheap, fast, and good. They got cheap upfront… and expensive later.

Example 2: “We Need It Yesterday”

A client comes in with urgency:

“We’ve left this late, we need it turned around immediately.”

Now we’re into speed.

To deliver quickly, the supplier has to:

- Reallocate resources

- Work overtime

- Push other jobs back

- Bring in more experienced (and expensive) people

The expectation, though? “Can you keep the price the same?” No. Because speed has a cost. If you want it done fast and done properly, it will not be cheap.

Example 3: The “Do It Properly… But Keep Costs Down” Brief.

This is probably the most common one.

“We want it done right. No issues. High quality. But we need to keep a tight budget.”

So what happens? The supplier adjusts:

- Longer timelines

- Careful resource planning

- Efficiency over urgency

You can get good and cheap. But you cannot get it quickly.

The Pattern Most People Miss

In every one of these situations, the same thing is happening: People believe they’re choosing all three:

- Fast

- Cheap

- Good

But in reality, they’re only ever getting two. The third doesn’t disappear, it just shows up later as a problem:

- Delays

- Extra costs

- Poor quality

- Stress

The Core Truth.

This is the part most people don’t say out loud: Every decision you make in business sits on a trade-off. Time, cost, and quality are constantly in tension. Push one, and something else has to move.

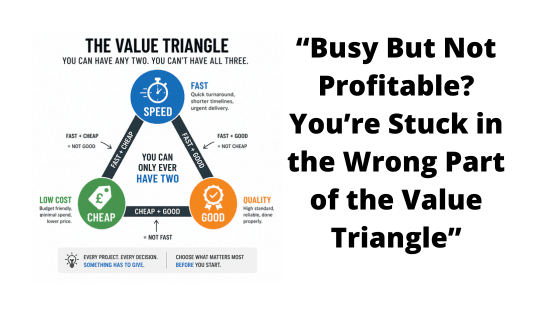

Introducing the Value Triangle.

This is where the Value Triangle comes in:

- Speed

- Cheap

- Good

You can have any two. You cannot have all three. Once you understand that, everything changes:

- Your expectations become realistic

- Your decisions become clearer

- Your conversations become easier

And most importantly: You stop paying for mistakes you didn’t even realise you were making.

2. What Is the Value Triangle?

At its simplest, the Value Triangle is a decision-making framework. It’s not theory. It’s not opinion. It’s how work actually gets delivered in the real world. Every project, every quote, every service sits somewhere within three competing forces:

- Speed

- Cheap

- Good

And here’s the part most people miss: These three don’t work together; they work against each other.

Breaking Down the Three Points.

Let’s strip this back to what each one really means in practice.

1. Speed (Fast)

This is about time.

- Quick turnaround

- Tight deadlines

- Urgent delivery

- Immediate response

In reality, speed means:

- More people on the job

- Longer working hours

- Priority over other work

Speed isn’t just about going faster. It’s about shifting resources to make it happen.

2. Cheap (Low Cost)

This is about price sensitivity.

- Lowest quote wins

- Budget constraints

- Cost control

- Value-engineering decisions

But “cheap” always involves trade-offs:

- Less experienced labour

- Reduced scope

- Minimal contingency

- Tighter margins

Cheap doesn’t mean efficient. It usually means something has been removed

3. Good (Quality)

This is about standards and outcomes.

- Done properly

- High level of skill

- Reliable delivery

- Attention to detail

To achieve “good,” you need:

- Experienced people

- Proper planning

- Time for execution

- Quality control

Good isn’t accidental. It’s the result of time, skill, and discipline.

The Constraint Nobody Talks About

Here’s where it all comes together. Each point puts pressure on the others.

- If you push for speed, costs increase

- If you push for low cost, time or quality drops

- If you demand high quality, you need either time or money

Which leads to the fundamental rule: You can have any two. You cannot have all three.

The Three Valid Combinations

Every project ends up in one of these:

- Fast + Good → Not Cheap

- Cheap + Good → Not Fast

- Fast + Cheap → Not Good

There isn’t a fourth option.

Why This Matters More Than People Think

Most problems in business don’t come from bad intentions.

They come from unclear expectations.

- The client thinks they’re getting all three

- The supplier knows they’re delivering two

- The gap between the two creates conflict

That’s where:

- Disputes start

- Margins disappear

- Relationships break down

A Simple Way to Think About It

Every time you make a decision, you’re answering one question:

Which two matter most?

- If it’s urgent and critical → Speed + Good

- If it’s budget-led but important → Cheap + Good

- If it’s quick and low cost → accept that quality will drop

Once that decision is made upfront, everything becomes easier:

- Pricing is clearer

- Delivery is smoother

- Expectations are aligned

The Shift Most Businesses Need to Make

The mistake I see over and over again is this:

Businesses try to position themselves as all three.

- Fast

- Cheap

- Good

And what actually happens?

They get dragged into:

- Price pressure

- Delivery stress

- Margin erosion

Clarity beats compromise. Every time.

This triangle isn’t just a concept.

It’s a tool.

And once you start using it properly, it changes how you:

- Price

- Sell

- Deliver

- And ultimately… how profitable your business becomes

3. Why This Triangle Exists (The Economics Behind It)

This isn’t a mindset issue. It’s not about optimism or negotiation. It’s economics. The Value Triangle exists because every business is constrained by three things:

- Time

- Resources

- Capability

You can flex them… but you can’t ignore them.

The Reality Most People Overlook

Every job you take on has a cost structure behind it. Not just the obvious costs like materials or labour, but the hidden ones:

- Management time

- Planning and coordination

- Risk and contingency

- Rework and quality control

- Opportunity cost (what you’re not doing instead)

When someone says: “Can you do it quicker, cheaper, and still keep the quality high?”

What they’re really asking is: “Can you remove the constraints of reality?”

And the answer is no.

3.1. Time Has a Cost

Speed is never neutral. To deliver something faster, you have to:

- Add more people

- Pay overtime

- Reprioritise work

- Interrupt existing workflows

That creates inefficiency. And inefficiency costs money.

Real Example:

A contractor has a 6-week schedule for a job. Client says: “We need it done in 3 weeks.” Now the contractor has to:

- Double labour

- Work longer hours

- Accept higher coordination risk

The cost doesn’t double neatly, it often increases disproportionately. Faster almost always means more expensive.

3.2. Skill Has a Cost

Quality comes from capability. And capability isn’t cheap.

- Experienced people cost more

- Specialists cost more

- Proven systems cost more

- Reliable suppliers cost more

If you want something done properly, you’re paying for:

- Fewer mistakes

- Better decision-making

- Smoother delivery

Real Example:

Two electricians quote the same job:

- One is highly experienced, charges more, and delivers clean work first time

- One is cheaper, less experienced, requires supervision and rework

The cheaper option often ends up costing more once:

- Snagging

- Delays

- Fixes

are factored in. Quality isn’t a feature, it’s an investment.

3.3 Low Cost Always Comes from Somewhere

This is the uncomfortable truth: Cheap is never free. It’s just hidden. If the price is low, one (or more) of the following has happened:

- Scope has been reduced

- Time has been extended

- Quality has been compromised

- Risk has been transferred

Real Example: A supplier wins work on a low price. But to make it work, they:

- Use less experienced labour

- Rush key stages

- Leave grey areas in the scope

The result? Variations, disputes, and “unexpected extras.” The buyer thought they were getting cheap. What they actually got was deferred cost.

3.4. The Compounding Effect

Here’s where it gets interesting. These factors don’t operate in isolation, they compound.

- Faster + High quality = premium cost

- Low cost + High quality = extended time

- Fast + Low cost = breakdown in quality

There’s no way around it because each decision puts pressure on the system. You’re not choosing outcomes, you’re choosing trade-offs.

3.5. The Role of Risk (The Hidden Fourth Factor)

Most people ignore this, but it’s critical. Every project carries risk:

- Delays

- Errors

- Unknowns

- External dependencies

When you push for:

- Faster timelines

- Lower costs

You’re increasing that risk. And when risk isn’t priced in properly? It shows up later as:

- Cost overruns

- Missed deadlines

- Margin erosion

Key Insight: If risk isn’t paid for upfront, it gets paid for later.

3.6. Why Businesses Get This Wrong

The biggest mistake I see isn’t misunderstanding the triangle. It’s ignoring it during the sales process. Businesses:

- Underprice to win work

- Overpromise on delivery

- Assume they’ll “figure it out later”

What actually happens?

- Margins disappear

- Teams get stretched

- Quality drops

You can break the triangle in the short term, but you pay for it in the long term.

The Bottom Line

The Value Triangle isn’t a theory. It’s a reflection of how businesses operate under constraint.

- Time costs money

- Skill costs money

- Certainty costs money

Remove one, and something else has to give.

The Commercial Insight

Once you understand the economics, everything becomes clearer:

- Pricing becomes easier

- Conversations become more honest

- Decisions become more deliberate

And most importantly: You stop chasing impossible combinations, and start building profitable ones instead.

4. The Three Real-World Combinations

This is where the Value Triangle stops being a concept and becomes real. Every job you’ve ever taken on, and every job you’ve ever bought, fits into one of these three combinations. Not sometimes. Not occasionally. Every time.

A. Fast + Good (Not Cheap)

This is the premium end of the market. You’re paying for:

- Urgency

- Expertise

- Reliability

And crucially, you’re paying for certainty.

What This Looks Like in Practice

- Emergency contractor called out at short notice

- Specialist brought in to fix a critical issue

- Project accelerated to meet a hard deadline

You’re not asking: “What’s the cheapest way to do this?”

You’re asking: “How do we get this done properly, right now?”

What It Requires Behind the Scenes

To deliver fast and maintain quality, the supplier has to:

- Prioritise your job over others

- Allocate their best people

- Work longer hours or add resources

- Absorb higher coordination pressure

That comes at a cost.

Real Example:

A manufacturing business has a production line down. Every hour costs thousands in lost output. They call in a specialist engineer.

- They arrive the same day

- Diagnoses the issue quickly

- Fixes it properly

The invoice is high. But no one argues because the alternative was far more expensive.

Key Insight: Fast + Good isn’t expensive, it’s valuable.

B. Cheap + Good (Not Fast)

This is the efficient, planned approach. You’re still getting quality, but you’re trading time to achieve it at a lower cost.

What This Looks Like in Practice

- Booking a reputable contractor months in advance

- Scheduling work during quieter periods

- Allowing proper planning and sequencing

The mindset here is: “I want it done properly, but I’m willing to wait.”

What It Requires Behind the Scenes

To keep costs down while maintaining quality, the supplier:

- Plans work efficiently

- Uses standard working hours

- Optimises resource allocation

- Avoids rush decisions

There’s less pressure, which means fewer inefficiencies.

Real Example:

A business is refurbishing an office. They’re not under time pressure. They choose a well-regarded contractor, not the cheapest, but not the fastest either.

- The work is scheduled over several weeks

- Materials are sourced properly

- The finish is high quality

The result? Good outcome, controlled cost, but it took time.

Key Insight: Cheap + Good works, if you remove urgency.

C. Fast + Cheap (Not Good)

This is the danger zone. It looks attractive at the start, but it’s where most problems begin.

What This Looks Like in Practice

- Lowest quote with a fast turnaround

- Promises that sound too good to be true

- Pressure to start immediately at a low price

The mindset is: “We need it done quickly, and we need to keep costs down.”

What Happens Behind the Scenes

Something has to give. And it’s almost always:

- Quality

- Attention to detail

- Proper planning

To hit both speed and price, the supplier is forced to:

- Cut corners

- Reduce scope

- Use less experienced labour

- Rush execution

Real Example

A business awards a project based on:

- Lowest price

- Fastest start date

Initially, everything looks fine. But then:

- Issues start appearing

- Snagging increases

- Deadlines slip

- Variations begin

The job ends up:

- Over budget

- Behind schedule

- Frustrating for everyone involved

Key Insight: Fast + Cheap is rarely cheap and never good.

The Pattern Across All Three

Here’s what’s important to understand: None of these combinations is “right” or “wrong.” They’re simply choices. The problem isn’t choosing the wrong combination. The problem is: Thinking you’re getting all three when you’re not.

Where Most Businesses Go Wrong

I see this constantly. Clients expect:

- Fast delivery

- High quality

- Low price

Suppliers:

- Agree to win the work

- Hope to manage the trade-offs later

That gap creates:

- Margin pressure

- Delivery stress

- Relationship breakdown

The Commercial Reality

Once you accept these three combinations, everything becomes clearer:

- You can position your business properly

- You can price with confidence

- You can manage expectations upfront

And most importantly: You stop getting pulled into deals that were never going to work in the first place.

5. The Hidden Cost of Trying to Get All Three

This is where most of the damage happens.

- Not at the start of the job.

- Not in the quote.

But in the gap between expectation and reality. Because when someone tries to get fast, cheap, and good, one of two things happens:

- The supplier says yes to win the work

- The client assumes it’s possible

And from that point on, the project is under pressure.

The Illusion at the Start

On paper, everything looks fine:

- The price is competitive

- The timeline is tight but “achievable”

- The quality expectation is clear

Everyone feels like they’ve won. But what’s actually happened is this: The trade-offs haven’t disappeared, they’ve just been hidden.

Where the Cost Really Shows Up

It doesn’t come through as one big problem. It shows up in small ways that compound over time.

5.1. Scope Gaps and “Grey Areas”

To hit a lower price, the scope gets tightened, sometimes subtly.

- Items excluded or vaguely defined

- Allowances instead of fixed costs

- Details left open to interpretation

At the start, it looks efficient. Later, it becomes:

- Variations

- Disputes

- “That wasn’t included” conversations

Cheap upfront often means expensive later.

5.2. Time Pressure and Rushed Decisions

When speed is forced into a low-cost model, something has to give. That something is usually thinking time.

- Less planning

- Faster decisions

- Shortcuts in sequencing

And that leads to:

- Mistakes

- Rework

- Inefficiencies

Rushed work rarely stays rushed; it just gets redone.

5.3. Quality Drift

No one sets out to deliver poor quality. But under pressure, standards start to slip:

- Less experienced people used

- Reduced supervision

- Shortcuts taken to stay on track

At first, it’s minor. Then it compounds:

- Snagging lists grow

- Issues get missed

- Final finish suffers

Quality doesn’t collapse all at once, it erodes over time.

5.4. Margin Pressure (The Silent Killer)

This is the one most businesses don’t talk about. When a supplier agrees to:

- Low price

- Fast delivery

- High expectations

They’re effectively agreeing to work under strain. Margins get squeezed. And when margins disappear:

- Corners get cut

- Decisions get reactive

- The focus shifts from delivery to survival

Unprofitable work is unstable work.

5.5. Relationship Breakdown

This is where it all ends up. Because when expectations aren’t aligned:

- The client feels let down

- The supplier feels squeezed

- Trust starts to erode

Conversations shift from:

- Collaboration

to:

- Defence

- Justification

- Blame

Most disputes aren’t about the work; they’re about misaligned expectations.

The Real Cost Isn’t Financial

Yes, there are cost overruns. Yes, there are delays. But the real cost is deeper:

- Time wasted

- Energy drained

- Opportunities missed

- Reputation damaged

And perhaps most importantly: Confidence is lost, on both sides.

A Pattern I See All the Time

A business wins work by being:

- Competitive on price

- Aggressive on the timeline

They deliver under pressure. Margins are tight. The team is stretched. Then they look at the numbers and think: “We’re busy… but where’s the profit?” This is usually why. They’ve tried to operate in all three corners of the triangle. And the business is paying the price for it.

The Brutal Truth

You don’t get fast, cheap, and good.

You get:

- Fast and cheap → and pay for quality later

- Cheap and good → and pay in time

- Fast and good → and pay upfront

But if you try to force all three? You pay in every direction.

The Commercial Insight

The most profitable, sustainable businesses don’t avoid this reality. They embrace it. They:

- Set clear expectations

- Price properly

- Position themselves honestly

And as a result:

- Their projects run more smoothly

- Their clients understand the trade-offs

- Their margins are protected

The Bottom Line

The hidden cost isn’t hidden at all. It’s just delayed. And by the time it shows up, it’s usually too late to fix easily. The smartest move you can make isn’t trying to get all three. It’s choosing the right two, on purpose.

6. How Smart Buyers Use the Triangle

Once you understand the Value Triangle, something shifts. You stop asking: “Can I get it fast, cheap, and good?” And you start asking:

“Which two actually matter for this decision?”

That’s the difference between reactive buying and deliberate decision-making.

The First Shift: From Hope to Clarity

Most buyers approach decisions with hope:

- Hope the cheapest option will still be good

- Hope the fast option won’t cost more

- Hope everything will just “work out”

Smart buyers don’t rely on hope. They make the trade-offs explicit upfront.

Step 1: Decide What Matters Most (Before You Speak to Anyone)

Before you even ask for a quote, you should be clear on one thing: What are you optimising for? Ask yourself:

- Is this time-critical?

- Is this budget-constrained?

- Is this quality-sensitive?

You don’t get to say “all three.” You have to choose.

Real-World Example

Let’s say you’re fitting out a new office.

- If you’ve already signed the lease and need to move in within 4 weeks, → Speed matters

- If cash is tight → Cost matters

- If this space represents your brand → Quality matters

A smart buyer prioritises: “We need this done properly, and we need to move in on time.” That’s Fast + Good. Which means they already know: It won’t be the cheapest option, and that’s fine.

Step 2: Communicate the Trade-Off Clearly

This is where most buyers go wrong. They say things like: “We’re looking for a competitive price, quick turnaround, and high quality.” That tells the supplier nothing. A smart buyer says:

- “We’re prioritising speed and quality, we understand that affects price.”

- “This is budget-led, but we still want a solid outcome; we’re flexible on timing.”

- “We need this quickly and within a budget. What’s realistically achievable?”

Now the supplier can respond properly. Clarity from the buyer creates clarity in the quote.

Step 3: Evaluate Quotes Through the Triangle (Not Just Price)

Most buyers make one critical mistake: They compare quotes purely on cost. Smart buyers compare based on:

- Position in the triangle

What This Looks Like in Practice

Instead of asking: “Why is this more expensive?” They ask:

- Is this quote faster?

- Is this quote higher quality?

- What’s being included that others aren’t?

They’re not just comparing numbers. They’re comparing trade-offs.

Example

Three quotes come in:

- £80k → Fast start, low detail

- £95k → Balanced, realistic timeline

- £120k → Fast delivery, highly detailed, strong team

A typical buyer goes for £80k. A smart buyer asks: “Why is the £120k option priced that way, and what risk does it remove?” That’s a completely different conversation.

Step 4: Accept the Consequence of Your Choice

This is where discipline comes in. Once you’ve chosen your two priorities, you have to stick to them.

- If you choose cheap + good, don’t complain about time

- If you choose fast + good, don’t push on price

- If you choose fast + cheap, accept the risk on quality

Most frustration comes from trying to change the rules halfway through. You can’t renegotiate the triangle after the decision is made.

Step 5: Use the Triangle as a Control Tool

Smart buyers don’t just use the triangle once; they use it throughout the project. When something changes, they revisit the trade-off:

- “If we bring the deadline forward, what happens to the cost?”

- “If we reduce the budget, what happens to quality?”

- “If we want higher quality, what does that do to the timeline?”

This keeps decisions grounded in reality.

The Big Advantage Smart Buyers Have

They don’t eliminate problems. They eliminate surprises.

- They understand what they’re paying for

- They understand what they’re not getting

- They make decisions with full visibility

And because of that:

- Projects run smoother

- Relationships stay intact

- Outcomes are more predictable

The Key Insight: The triangle doesn’t limit you; it gives you control.

Most buyers feel constrained by it. Smart buyers use it to:

- Make better decisions

- Have better conversations

- Get better outcomes

The Bottom Line

Every buying decision is a trade-off. The difference is:

- Average buyers make those trade-offs accidentally

- Smart buyers make them deliberately

If you want better outcomes, don’t try to beat the triangle. Use it.

7. How Smart Businesses Sell Using the Triangle

This is where the Value Triangle becomes powerful. Most businesses treat it as a constraint. Smart businesses use it as a sales tool.

The Big Shift: Stop Trying to Be All Three

The biggest mistake I see is this: Businesses try to position themselves as:

- Fast

- Cheap

- Good

At the same time. It sounds attractive. But in reality, it creates:

- Confusion in the market

- Pressure on pricing

- Constant negotiation

Because the customer doesn’t believe it. And deep down, neither do you. If you try to be everything, you end up competing on price.

Step 1: Choose Your Position in the Triangle

Every strong business makes a deliberate choice: Which two are we known for? Not occasionally. Not “when needed.” Consistently.

Three Clear Market Positions

1. Fast + Good (Premium Positioning)

This is where you compete on:

- Expertise

- Responsiveness

- Reliability

You are the solution when: “It has to be done properly, and it has to be done now.” You don’t apologise for the price. You justify it.

2. Cheap + Good (Value Positioning)

This is where you compete on:

- Efficiency

- Planning

- Consistency

You are the solution when: “I want it done properly, but I’m prepared to wait.” You don’t promise speed. You promise value over time.

3. Fast + Cheap (Volume Positioning)

This is where you compete on:

- Speed

- Accessibility

- Simplicity

You are the solution when: “I need something done quickly, and I need it at a low cost.” But here’s the reality: You are not selling perfection. You are selling convenience.

Step 2: Make the Trade-Off Explicit in Your Sales Process

Most businesses avoid this conversation. Smart businesses lead with it. Instead of saying: “We’re competitive, high-quality, and responsive…”They say:

- “We focus on delivering high-quality work quickly, which means we’re not the cheapest option.”

- “We deliver excellent work at a fair price, but we don’t rush jobs.”

- “We can turn this around quickly and cost-effectively, but it won’t be a premium finish.”

This does two things immediately:

- It builds trust

- It filters the wrong clients out

Clarity attracts the right clients and repels the wrong ones.

Step 3: Control the Conversation (Instead of Defending Price)

Most businesses get dragged into this: “Can you do it cheaper?” Because they haven’t framed the trade-off. Smart businesses respond differently. They bring it back to the triangle:

- “If we reduce the price, we’d need to adjust either the timeline or the scope, what would you prefer?”

- “We can absolutely bring the cost down, but that would mean extending the delivery time.”

- “If you need this quicker, we can do that, but it will impact the cost.”

Now the conversation isn’t about price. It’s about choices. You move from defending your price to guiding a decision.

Step 4: Protect Your Margins Without Saying “No”

This is where the triangle really earns its keep. Instead of saying:“No, we can’t do that.” You say: “Yes, but here’s what changes.”

- Lower price → longer timeline

- Faster delivery → higher cost

- Higher quality → increased investment

You’re not resisting the client. You’re educating them. And that changes the dynamic completely.

Step 5: Build Your Brand Around Your Position

The strongest businesses don’t just choose a position; they own it.

- Premium providers lean into speed and quality

- Value providers lean into quality and efficiency

- Volume providers lean into speed and price

Everything aligns:

- Messaging

- Pricing

- Delivery

- Client expectations

That consistency builds:

- Trust

- Reputation

- Pricing power

Real-World Example

Think about your own buying behaviour. When something matters, you don’t look for the cheapest. You look for:

- Someone who knows what they’re doing

- Someone who can deliver when needed

And you accept the cost. Why? Because the risk of getting it wrong is higher than the price. That’s exactly where you want your business positioned.

The Mistake That Destroys Profitability

Businesses say: “We need to be competitive.” What they mean is: “We need to be cheaper.” And that’s where the spiral starts:

- Lower prices

- Tighter margins

- More pressure

- Worse outcomes

All because they haven’t defined their position in the triangle.

The Commercial Insight

Positioning isn’t what you say, it’s what you’re willing to trade off.

Smart businesses understand this. They don’t try to win every job. They win the right jobs.

The Bottom Line

The Value Triangle isn’t just about delivery. It’s about how you sell.

- It gives you language

- It gives you control

- It gives you positioning

And most importantly, it allows you to charge properly for the value you deliver.

8. The Pricing Conversation Most Businesses Avoid

This is the part that separates average businesses from profitable ones. Not delivered. Not marketing. The conversation. Because most businesses don’t lose money on bad work. They lose money on bad conversations before the work even starts.

The Conversation That Never Happens

Here’s what typically happens: A client says, “We need it quickly, done properly… and at a competitive price.” And instead of challenging that, the business responds with: “Yes, we can do that.”

At that moment, the deal is already broken.

- Not visibly.

- Not immediately.

But structurally. Because you’ve just agreed to something that can’t exist.

Why Businesses Avoid This Conversation

Let’s be honest, this isn’t about knowledge. Most business owners instinctively understand the trade-off. They avoid the conversation because:

- They don’t want to lose the job

- They don’t want to create friction

- They think they’ll “figure it out later”

So they:

- Underprice

- Overpromise

- Hope delivery will somehow make it work

It rarely does.

What This Creates Instead

When you don’t address the triangle upfront, the pressure doesn’t disappear. It just moves. And it shows up as:

- Price objections later

- Scope creep

- Unrealistic expectations

- Margin erosion

- Stress in delivery

You haven’t avoided the conversation; you’ve delayed it. And delayed conversations are always harder.

What Smart Businesses Do Differently

They don’t avoid the conversation. They lead it. Early. Clearly. Professionally.

They Make the Trade-Off Visible

Instead of trying to satisfy everything, they say:

- “We can absolutely deliver this quickly and to a high standard, but it won’t be the lowest cost option.”

- “If keeping costs down is the priority, we can do that, but we’ll need more time.”

- “If you need this quickly and within budget, we’ll need to simplify the scope.”

Notice what’s happening here:

- No resistance

- No defensiveness

- No discounting

Just clarity.

They Reframe the Pricing Discussion

Most businesses get pulled into: “Why are you more expensive?” Smart businesses shift it to: “What are you actually trying to achieve?” Now the conversation becomes:

- Outcome-focused

- Trade-off-based

- Rational

Instead of being emotional and price-driven.

They Use the Triangle to Guide the Decision

When a client pushes on price, they don’t panic. They guide. For example:

Client: “Can you bring the price down?”

Response: “We can look at that. If we reduce the cost, we’d need to either extend the timeline or adjust the scope. Which would you prefer?”

Now the client is making a decision. Not just asking for a discount. You’ve turned a price objection into a structured choice.

They Stay in Control of the Deal

Here’s the key difference:

- Average businesses react

- Smart businesses frame

They don’t get dragged into negotiation. They define the terms of it. That creates:

- Respect

- Trust

- Better clients

Real-World Example

A client pushes for:

- Fast turnaround

- High quality

- Lower price

An average response: “We’ll see what we can do…”

A smart response: “We can deliver this quickly and to the standard you’re expecting. If we reduce the price, we’d need to adjust either the timeline or the level of finish. Which is more flexible for you?”

Same situation. Completely different outcome.

Why This Works

Because it does three things:

- Educates the client: Most clients don’t think in trade-offs until you show them

- Positions you as an expert: You’re not selling, you’re advising

- Protects your margins: You don’t give away value, you exchange it

The Key Line to Remember

If you take nothing else from this section, take this: “We can absolutely do that, but something else has to change.” That one line keeps you:

- Honest

- In control

- Profitable

The Commercial Insight

The pricing conversation isn’t about defending your number. It’s about defining the terms of the decision. Once the client understands the triangle:

- Price becomes logical

- Trade-offs become acceptable

- Decisions become easier

The Bottom Line

Most businesses avoid this conversation because they think it will cost them the sale. In reality, avoiding it costs them profit.

If you want to improve your pricing, don’t start with numbers. Start with the conversation.

9. The Link to Profitability and Business Value

This is where the Value Triangle stops being operational, and becomes financial. Because how you position yourself within the triangle doesn’t just affect how you deliver work. It directly determines:

- Your margins

- Your consistency

- Your stress levels

- And ultimately… what your business is worth

Most Businesses Think This Is About Projects

It’s not. It’s about the pattern of behaviour. If your business consistently tries to deliver:

- Fast

- Cheap

- Good

You’re not just making a mistake on one job. You’re building a model that destroys profit over time.

The Margin Problem Starts Here

Let’s break it down simply. If you:

- Compete on price (cheap)

- Accept tight deadlines (fast)

- Try to maintain standards (good)

You’re absorbing the cost of all three. But only getting paid for one. That gap is where your margin disappears.

Real Example: Busy But Not Profitable

I see this constantly. A business is:

- Winning work

- Delivering projects

- Keeping teams busy

But when we look at the numbers:

- Margins are thin

- Cash is tight

- Profit is inconsistent

Why? Because they’re operating in the impossible zone of the triangle. They’ve built a business that:

- Underprices to win work

- Overdelivers to maintain reputation

- Rushes to meet deadlines

They’re working harder, but earning less.

Pricing Power Comes From Positioning

This is the shift most businesses need to make. Profitability isn’t just about:

- Cutting costs

- Improving efficiency

It’s about pricing power. And pricing power comes from clarity of position in the triangle.

Fast + Good Businesses

- Command premium pricing

- Justify it through urgency and expertise

- Protect margins through value

Cheap + Good Businesses

- Maintain steady margins

- Optimise through efficiency and planning

- Avoid costly rush and rework

Fast + Cheap Businesses

- Survive on volume

- Accept lower margins by design

- Rely on systemisation, not craftsmanship

The Problem Is When You Drift Between Them

This is where most businesses lose control. They:

- Price like a “cheap” provider

- Deliver like a “good” provider

- Operate under “fast” conditions

That combination is lethal. You’re delivering premium work at discount prices under pressure. There’s no margin in that.

The Link to Business Value

Now let’s take this one step further. Because this isn’t just about profit today. It’s about what your business is worth tomorrow.

Buyers Don’t Just Look at Profit

They look at:

- Consistency of profit

- Predictability of revenue

- Strength of pricing

- Reliability of delivery

And all of those are shaped by your position in the triangle.

Two Businesses, Same Profit, Different Value

Let’s say two businesses both make £200,000 profit.

Business A

- Constantly discounting

- Fighting price pressure

- Dealing with rework and delays

- Margins fluctuate

Business B

- Clear positioning (Fast + Good, for example)

- Strong pricing discipline

- Consistent delivery

- Predictable margins

On paper, they look the same. In reality, they’re not even close. Business B will be worth significantly more.

Why?

Because buyers don’t just buy profit. They buy certainty of profit.

Where the Triangle Drives Valuation

If your business is clear in its position:

- Pricing is consistent

- Margins are stable

- Delivery is predictable

- Risk is lower

That leads to:

- Higher multiples

- Stronger buyer confidence

- Better exit options

If You Ignore It

If you operate across all three corners:

- Pricing is inconsistent

- Margins are volatile

- Delivery is unpredictable

- Risk is higher

That leads to:

- Lower multiples

- Buyer hesitation

- Discounted valuations

The Key Insight: The triangle isn’t just a delivery model, it’s a valuation driver.

The Commercial Reality

You don’t build a valuable business by:

- Winning more work

- Cutting more costs

You build it by:

- Choosing the right position

- Sticking to it

- Pricing accordingly

The Bottom Line

If your business feels:

- Busy

- Stretched

- Under pressure

But not as profitable as it should be…There’s a strong chance you’re trying to sit in all three corners of the triangle.

Clarity in position creates consistency in profit. Consistency in profit creates value.

10. Final Word – You’re Always Choosing (Whether You Realise It or Not)

Most people think the Value Triangle is something you apply occasionally. It’s not. It’s something you’re using every single day, whether you’re aware of it or not.

Every Decision Is a Trade-Off

Every time you:

- Price a job

- Accept a deadline

- Agree a scope

You’re making a choice between:

- Speed

- Cost

- Quality

Even if you don’t say it out loud.

The Problem Isn’t the Triangle

The triangle isn’t the issue. It’s not a limitation. It’s not something to work around. The problem is pretending it doesn’t exist. Because when you ignore it:

- You agree to unrealistic expectations

- You underprice work

- You overpromise on delivery

- You create pressure before the job even starts

And that pressure always shows up somewhere:

- In your margins

- In your timelines

- In your quality

- Or in your relationships

You’re Already Making the Choice

This is the key point. You don’t get to opt out. You’re already choosing:

- When you discount to win work → you’re choosing cheap

- When you accept tight deadlines → you’re choosing fast

- When you promise high standards → you’re choosing good

The only question is: Are you choosing deliberately, or accidentally?

What Changes When You Take Control

When you start using the triangle properly, everything tightens up.

- Your pricing becomes clearer

- Your conversations become easier

- Your delivery becomes more consistent

And most importantly: Your business becomes more predictable and more profitable

The Shift From Reactive to Deliberate

Most businesses operate like this:

- React to the client

- Adjust to pressure

- Compromise to win work

Smart businesses operate differently:

- Define their position

- Set expectations early

- Stick to the trade-offs

That’s the difference between:

- Constant firefighting

- And controlled growth

The Real Advantage

This isn’t about saying “no” more often. It’s about saying yes properly.

- Yes, we can do it quickly—but not cheaply

- Yes, we can keep costs down—but it will take longer

- Yes, we can deliver high quality—but it requires investment

That level of clarity does two things:

- It builds trust

- It protects your business

The Final Thought

You can have any two. You cannot have all three.

That’s not a limitation. That’s a framework. And once you start using it:

- You make better decisions

- You attract better clients

- You build a stronger, more valuable business

The Bottom Line

You’re always choosing. Whether you realise it or not. The difference between struggling businesses and successful ones isn’t the work they do. It’s the decisions they make before the work even starts.

Your Next Step – Pricing Audit

If your business feels busy… but not as profitable as it should be, there’s usually a reason. You’re sitting in the wrong part of the triangle.

- Pricing like you’re cheap

- Delivering like you’re premium

- Operating under constant time pressure

That combination will drain margin, every single time.

The Reality

Most businesses don’t have a sales problem. They have a pricing and positioning problem. And until you fix that, no amount of extra work will improve the bottom line.

What the Pricing Audit Does

This isn’t theory. It’s a structured review of how your business actually prices, sells, and delivers. We look at:

- Where you currently sit in the Value Triangle

- Where your margins are being lost

- How your pricing is being interpreted by the market

- The signals your customers are giving you (and what they really mean)

And most importantly: What needs to change to improve profitability quickly and practically

What You’ll Walk Away With

- A clear view of your pricing position

- Identified margin leaks

- Practical steps to improve pricing confidence

- A structured plan you can act on immediately

No fluff. No theory. Just clarity.

The Next Step

If you want to understand why your pricing isn’t delivering the results it should:

Book a Pricing Audit session. (Hit the button below)

We’ll go through your business together and identify exactly where the issues are and how to fix them.

Final Line: You don’t fix profit by working harder. You fix it by pricing smarter.

Note: This is provided by our Sister company Rule29 Ltd.